Mirovα, Creating Sustainable Value - October 2024

Monthly market review and outlook

US resilience amid Chinese surprise

In the span of a month, the markets have given us the impression of going through a complete cycle with investor perceptions shifting from one extreme to another over the period. September got off to a poor start, but ended the month with a clear rebound. The S&P 5001 gained 2%2, making it the best month of September in five years, while the global bond index gained 1.7%2, buoyed in particular by a 1.2%2 rise in US Treasuries, marking the fifth consecutive monthly increase since 2010.

September is traditionally a difficult month for the markets, and 2024 seemed to be no exception. Very disappointing data from the eurozone dampened investor spirits, with the manufacturing PMI3 still in contraction mode at 45.82 points, weighed down by a fall in the new orders component and the announcement of job cuts, particularly in the case of Volkswagen in Germany. Overall, business confidence continues to erode. As for France, fears relate to the deficit, which is expected to exceed 6%2. During the month, the 10-year spread4 between France and Germany reached 802 basis points, despite Germany's difficulties. Since the dissolution of the National Assembly, the French spread has risen by 35 basis points against Germany and Greece, and by 252 basis points against Spain. France is now borrowing on the same terms as Spain and at more expensive terms than Portugal.

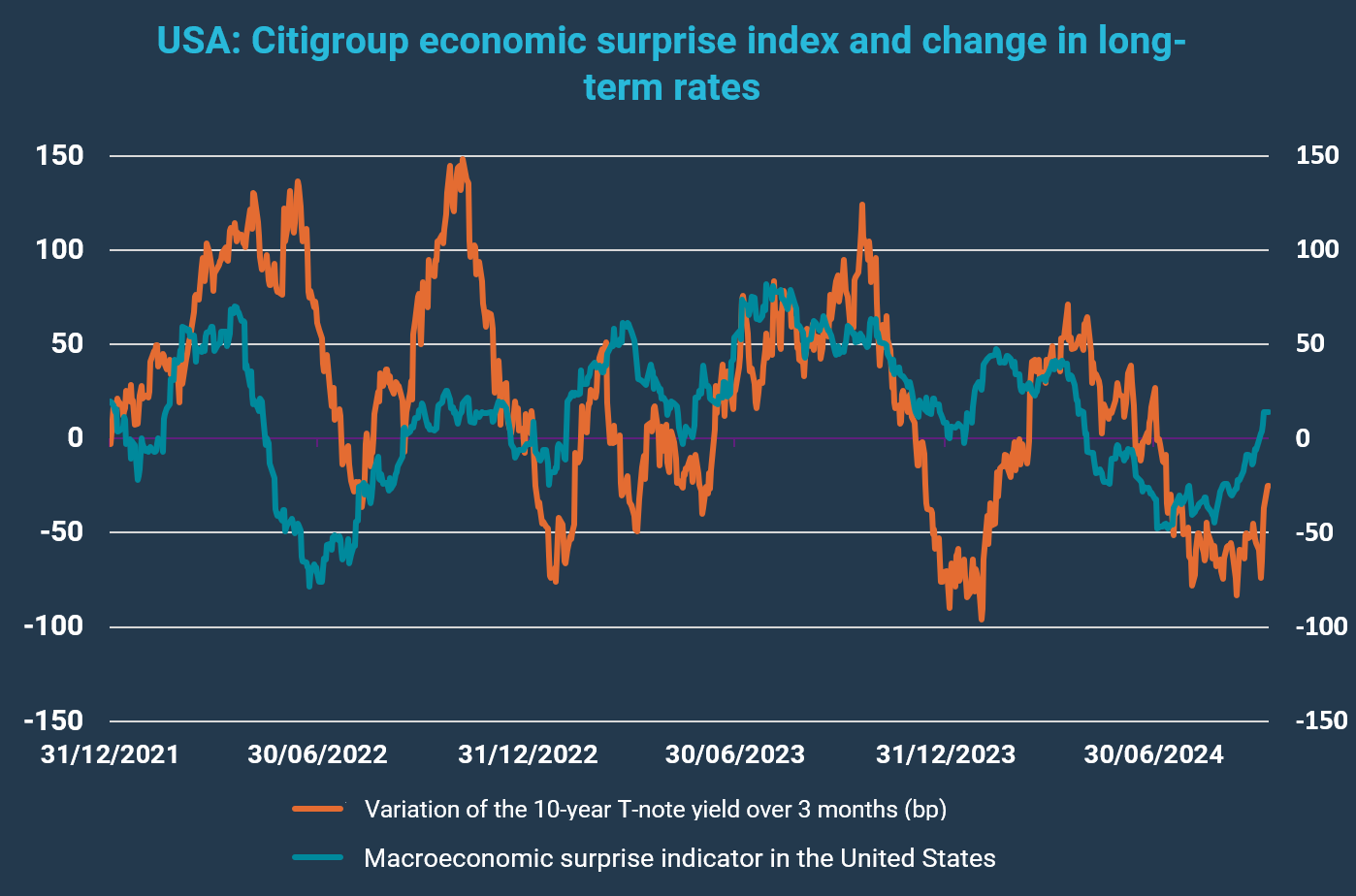

The bullish rally in risky assets must therefore be sought outside the eurozone, and more specifically in the United States and China. Across the Atlantic, the Federal Reserve's rate cut came as something of a surprise in terms of its size (50 basis points2), but at the same time the institution succeeded in sending out positive signals about the health of the US economy. The decision was taken almost unanimously by the members of the Board of Governors, notably to counter a possible slowdown in the employment market. But the Fed5 insisted on the preventive aspect of its decision, indicating that it was acting in anticipation rather than reaction, in order to consolidate the soft landing scenario and avert any risk of recession. In this respect, the 140,000 jobs2 reported in September for the month of August were reassuring after the stress of the summer. This was subsequently confirmed by the figures published in October, which were well above expectations (see macro outlook below). On top of this, inflation is still falling, and is gradually moving towards the 2%2 target in line with the Fed's objectives. Consumer confidence is holding firm, while the political contest seems to be turning in Kamala Harris's favour. Leading in the polls in a majority of swing states and nationally, her victory could have a limited effect on inflation, unlike that of her opponent.

In the markets, the 2-year yield fell sharply, by 27 bps6, while the decline in the 10-year yield was less pronounced, falling 12 bps2, which reinforced the steepening of the curve. This easing has benefited cyclical stocks, construction, consumer discretionary, basic industries and the automotive sector.

The ECB7 also cut its key rate by 252 basis points, as expected by the market. The real surprise, however, came from China. At the Politburo meeting in September, the Chinese authorities sought to demonstrate their determination to regain control of the country's economic situation, based on a "whatever it takes" policy. Although not on the scale of the recovery from the 2008 crisis, the authorities nevertheless appear ready to deploy all the means necessary to halt the fall in the property market and stimulate asset prices in order to halt the confidence crisis into which the country has sunk. Beijing has therefore announced a massive monetary and fiscal stimulus plan, which is designed to support consumption, the banking system through recapitalisations, the construction and property sectors through interest rate cuts and the purchase of unsold stock, and the equity markets through unprecedented measures. The markets reacted almost immediately, gaining almost 25%8following the announcements. The effects of this plan were also felt on the European stock markets, with a rebound in luxury goods and basic materials stocks.

Despite this major stimulus package and the rebound in cyclical stocks, oil fell by 9%9 over the month. This is due to Saudi Arabia's decision to abandon its targets for reducing oil production. The fall in oil prices has reinforced the consumption theme in the markets. Finally, bitcoin ended the month up by 108.

Graph of the month

Macro review and outlook

Macroeconomy: one month before the US elections, eyes turn to China

After a very good third quarter, what does the end of the year hold in store? In the markets, the prevailing view remains that the global economy is generally operating at its true potential, in line with growth of around 3%9, despite an explosive geopolitical context and a wait-and-see attitude ahead of the US elections. Activity in the United States is proving more resilient than expected, with economic surprise indexes moving from negative to positive. Our scenario in favour of a successful US soft landing is therefore confirmed for the time being. The areas to watch are the eurozone, with France and Germany mired in economic and political difficulties, and China, where we will have to assess the effects of the stimulus announcements over time.

United States: the right dosage by the Fed

The Fed board was virtually unanimous in its support for a 50-cent rate cut: this momentum proves that the institution is paying close attention to the US employment figures and is fairly confident that the disinflation dynamic will continue. After what we believe was an exaggerated warning (see Mirova, Creating sustainable value of september) in August, the Federal Reserve's priority remains the health of the labour market. Its aim is to take preventive action to avoid triggering waves of redundancies. History shows that once initiated, these trends are extremely difficult to reverse, hence the 50 basis point10 rate cut, which was higher than the consensus.

The market appreciated this decision all the more because, traditionally, a cycle of monetary policy easing during a soft landing rather than a recession is very favourable for risky assets, particularly equities. However, it should be noted that the Fed's expectations for rate cuts over the next few quarters are still aggressive, so there is a risk of potential retracement in the event of a rebound in activity, similar to the movement at the beginning of October following job creation figures that were well above the consensus view. Our central scenario remains that of two 25bps9 rate cuts between now and the end of the year, in November and December, as well as a gradual reduction between now and next summer towards a final rate of around 3.59.

The market is also in favour of the political scenario of Kamala Harris winning the election and one of the two Houses being won by the Democrats. This scenario seems to be the most likely but still very uncertain (due to the risk of a potential shock to post-election interest rates). This provides reassurance in the face of the spectre of inflationary policy measures and trade tensions, which are highly plausible in the event of Donald Trump's victory.

Finally, the American consumer, the key focus of attention, seems confident. It has benefited from the fall in oil prices and a positive wealth effect, from a gain in real purchasing power and from a savings reserve which, in the end, turns out to be significantly higher, in aggregate, than the initial consensus estimates, which were betting on the disappearance of post-covid surpluses.

Annualised GDP9 growth in the third quarter was almost 3%9 according to the Atlanta Fed's model. The United States could therefore record growth of 2.7-2.8%9 over the year, with growth potential already established for 2025. Also, the consensus still puts the probability of a recession over the next 12 months at 30%9, which we think is too high.

Euro Zone: France and Germany are a cause for concern

While the bad news from the eurozone seems to have been taken on board by the market, there are still many areas of concern, and we will probably have to wait until the second half of 2025 to see a rebound. The two main stumbling blocks are to be found in France, with a deficit that needs to be reduced, and in Germany, with an industrial recession, while the margins for manoeuvre are shrinking for another year. These two countries are a far cry from the more enviable situation in Spain, which is reaping the benefits of productivity gains, re-industrialisation, a falling deficit, the positive effects of immigration and EU stimulus packages.

France in particular is at the heart of all the concerns, with an unstable political situation, and this at a time when the EU10 is expecting it to reduce its deficit sharply. GDP growth over 2024 is expected to be 1.2%11, but should fall back to 1% at best from next year, with private investment rebounding very slowly. Moreover, investment momentum was very weak in the second quarter, and growth was revised from 0.3% to 0.2%11.

What's more, the nature of growth this year has not been conducive to reducing deficits. This was due to a rise in exports outside the eurozone and a fall in imports, as consumption slowed. There is therefore no sale of taxable products to bring tax revenue into the state coffers. Now, to avoid a debt crisis scenario, the government has to find the right balance between cutting spending and raising taxes, so as not to undermine growth. As we noted in April, the only good news in this respect comes from a range of economies which, in theory, have little impact on growth. No doubt this explains why, for the time being, French debt is not under attack from investors. However, the risk of the situation being reversed cannot be ruled out, particularly in the event of a motion of censure being adopted against the government or the pension reform being repealed.

Faced with this situation, we do not see any factors that could give rise to a short-term positive surprise in France, and the favourable scenarios tend to focus on Spain and Italy, for reasons that are less homogeneous than might appear. France's spread could therefore continue to diverge from that of other European countries.

ECB under pressure

The ECB has also cut rates again, while inflation in France, Germany, Italy and Spain has fallen below expectations, to under 2%11. This is partly due to a very low energy component and favourable base effects compared to a year ago. However, the extent of the downturn goes beyond these base effects alone, with year-on-year inflation levels coming in half a point below expectations, including the estimates made by the ECB.

With a fall in confidence and the leading indicators, as well as a manufacturing recession in Germany and France, we do not expect growth in the eurozone to rebound in the short term. The ECB is therefore set to continue cutting rates by 25 basis points in October and December. By mid-2025, it should converge towards its neutral rate of 2%11, a threshold that we believe is necessary given the economic environment. The economic situation is putting the ECB under pressure and subjecting its decisions to intense scrutiny. It could also accelerate the pace of rate cuts if the Fed follows a similar path.

China takes the world by surprise

Xi Jinping took the floor in person to present the country's extensive fiscal and monetary stimulus package. While this is surprising in terms of its scale, it is most notable for its deployment of new support levers. Consequently, the government plans to take direct action with the poorest sections of the population by distributing cheques, which is an unusual initiative. It is also supporting the markets by facilitating share buybacks and allowing ETFs12 to be used as collateral to obtain credit. The government, which is seeking to halt a negative wealth effect for its population, has also launched a raft of measures designed to support the property market. As well as lowering interest rates and easing credit conditions, it also wants to support local authorities in their efforts to buy up their unsold property stocks, in order to stimulate the market. Success in this area will be key to the future direction of the Chinese economy.

This plan demonstrates a willingness to intervene "whatever it takes" and suggests further rate cuts if necessary. This will also attempt to dissuade investors from shorting China on the markets. Furthermore, they have been responsive to the Chinese announcements. The market, which had been largely underweight on Chinese equities, has returned to a more neutral stance.

The effects of the plan to be monitored

The Chinese authorities did not provide a detailed breakdown of the aid to be deployed. Some figures have leaked to the press, but the scale of the budgeted package and the implementation of the measures need to be closely monitored. Perhaps this vagueness also serves to retain levers that can be activated if necessary after the US elections, the outcome of which could prove more or less favourable to China depending on whether Mr Trump wins a second term or Mrs Harris wins one. This comes at a time when the yuan has appreciated over the summer and the Fed's accommodating policy is easing the pressure on emerging markets, with lower interest rates and a weaker dollar. Nevertheless, beyond this rather judicious timing, the impact of the plan on domestic demand will need to be carefully measured, and its effects on the real economy, particularly property prices, will need to be validated. On a wider scale, the aim is also to avoid the flight of foreign capital, in both the short and long term. We believe that Mr Xi's announcements, given the scale of the measures proposed, will have a beneficial effect, but it is hard to see how this could last beyond the end of 2025, given that China's underlying macroeconomic fundamentals seem to have been damaged by its demographics.

What about the US elections?

Everyone has their perspectives on the US elections and their potential implications. We are also engaging in this discussion, making a clear distinction between the scenario of a Mr Trump victory with a majority in both Houses of Congress, that of a Mr Trump victory without control of these two Houses, and that of Mrs Harris entering the White House. However, the most important prediction, in our view, is that this election will do little to change the fortunes of the US economy, the real drivers of which we believe are still to be found in Palo Alto, Texas, in factories across the country rather than in Washington. Over the past two years, we have written at length about the reasons for our optimism about the future of the US economy, based above all on the productivity gains to be derived from the rejuvenation of the US industrial base, combined with the implementation of robotics and even artificial intelligence. We fail to see why the Democrats or the Republicans would be bent on stopping this process, unless they want to back it up with fiscal expansionism, which we now believe is too complicated for the Treasury, or even the FED, to absorb given the deficit levels already reached. The major issue is that these elections will undoubtedly have a significant influence... outside the United States, which remains a fairly closed economy, and paradoxically a very important one for many economies such as Germany, Italy, China and many others. The Middle East conflict situation, with Trump more aggressive than the Democrats on Iran, or in Ukraine, with a possible Harris administration undoubtedly more offensive than the Republicans towards Russia, will also change depending on who occupies the Oval Office. To paraphrase John Connally, who said to European diplomats that "the dollar is our currency, but your problem", we could say of the Americans that "the host at the White House is their President, but not their problem". Here lies the source of our unwavering optimism about the United States: this does not mean the programme of Mr Trump would not have any influence on the US economy, but that this influence would not jeopardize the mega trends currently at work there.

The Long View

Banks – Look further East

Navigating Investment Challenges

The narrowing of spreads between banks in peripheral Europe13 and core14 countries has presented investors with a challenge in finding new investment opportunities with a strong credit story and potential for spread compression. Amongst the alternatives are the possibilities i) to move down the capital structure, ii) lengthen maturities, or iii) invest in lower-rated issuers to capture higher yields. However, for investors who are unable or unwilling to take on more risk due to portfolio constraints, we argue that investing in bonds issued by Central and Eastern European (CEE) banks offers a compelling opportunity to increase portfolio yield without compromising overall risk and volatility.

Overview of the CEE Banking Sector

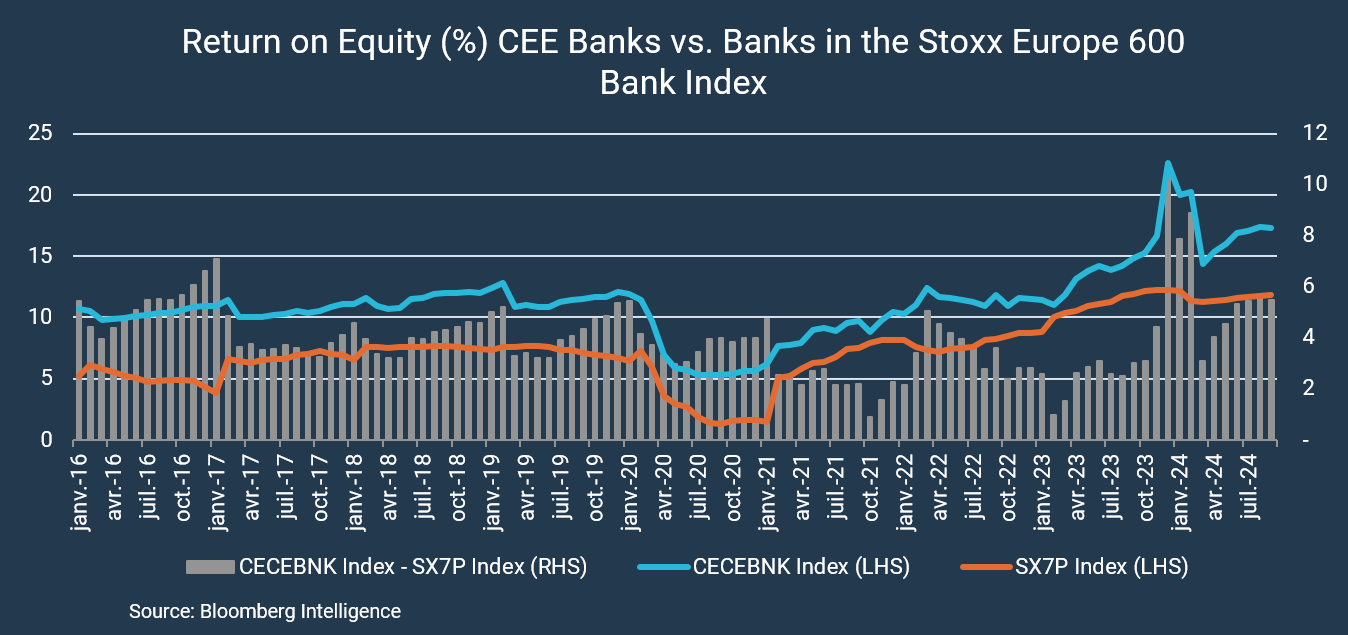

The banking sector in CEE represents a relatively small proportion of the European Union (EU) banking assets, accounting for approximately 5%15 of the total as of the end of June 2024. Poland and Czech Republic are the largest contributors to this proportion. CEE banks present an appealing opportunity for investment in growing European emerging economies that benefit from EU membership and its institutional framework. We consider the CEE banking systems are profitable, well capitalised, have adequate asset quality broadly in line with that of European peripheral banks and stable domestic deposits as a funding source. However, there are downside risks to consider, amongst which political instability in some countries and geopolitical risks, particularly for the Baltics. Additionally, in certain countries like Poland and Hungary, high government interventionism in the banking sector has led to measures aimed at supporting borrowers, which have put pressure on banks' profitability. Nevertheless, banks have demonstrated resilience in absorbing these measures and have remained profitable.

Growing Investment Universe

We limit the investment space for CEE banks to the 11 EU member countries in the region. Within this universe, there are about 30 banks that have issued less than 100 senior and subordinated bonds denominated in EUR, each with an outstanding amount exceeding €100m16. Approximately two-thirds of these bonds are rated by at least one rating agency and were primarily targeted at international investors. The total outstanding nominal amount of the rated universe is slightly above €20bn, with a concentration in the Czech Republic, Poland, and Hungary, followed by Romania and Slovenia, Slovakia, and Estonia. The average nominal size is below benchmark size, i.e. €500m.

The green, social and sustainability bonds (GSS) issued by CEE banks in Mirova's investment universe exhibit an eligibility ratio of about 45%16, compared to around 75%16 for all banks in our database. Two primary reasons account for this eligibility gap: CEE banks often lack a robust decarbonisation strategy, including specific targets for carbon emissions reductions within their loan portfolios. However, this gap is narrowing, as several CEE financial institutions have recently begun to adopt criteria from the EU green taxonomy, which aims to maximise the impact of projects and assets supported by green bonds.

Regulation Drives Debt Issuance

In recent years, CEE banks have primarily issued senior preferred (SP) and non-preferred (SNP) instruments to comply with EU regulations, particularly the Minimum Requirement for Own Funds and Eligible Liabilities (MREL), which requires banks to maintain eligible debt instruments for orderly resolution and capital restoration in case of non-viability. Most of the regulatory-driven issuance needs have already been met, creating a positive supply effect for existing bonds. Future issuance will depend on factors such as balance sheet growth, evolution of risk-weighted assets, and specific rules in certain countries, such as Poland where banks need to issue wholesale debt to comply with a new long-term financing regulation17. Subordinated bond issuance for foreign-owned banks typically occurs at the parent level or on the domestic market. Smaller banks are generally using own funds to comply with MREL. The European Bank for Reconstruction and Development (EBRD) is a long-term investor in CEE banks, which we view as a stabilising factor in the market.

Investment Grade Universe

The euro-denominated senior instruments issued by CEE banks are predominantly rated as Investment Grade, with ratings ranging from BBB- to A- and only few bonds rated High Yield, whereas the EU average sits around A-/A. In some cases, these ratings benefit from the support provided by the foreign parent of the bank. The banking sectors in CEE are largely foreign-owned, primarily by Western European banks, which are attracted by the high risk-return and solid growth prospects in the region relative to the more limited headroom in their home countries where they already enjoy dominant positions. Austrian banks, such as Raiffeisen Bank International SA (RBI) and Erste Group Bank AG, are particularly active in the CEE market, leveraging their geographic proximity to establish large CEE operations with leading local franchises in selected countries. The Belgian KBC Group NV also has extensive footfall in four CEE countries. In fact, more than 40% of the former’s 1H24 consolidated revenue was generated in CEE countries. Additionally, other major European banks, including ING Groep N.V., UniCredit SpA, and Intesa Sanpaolo SpA, are also selectively growing their presence in the region, indicating the attractiveness of the CEE banking sector for foreign institutions.

Premium Versus European Peripherals

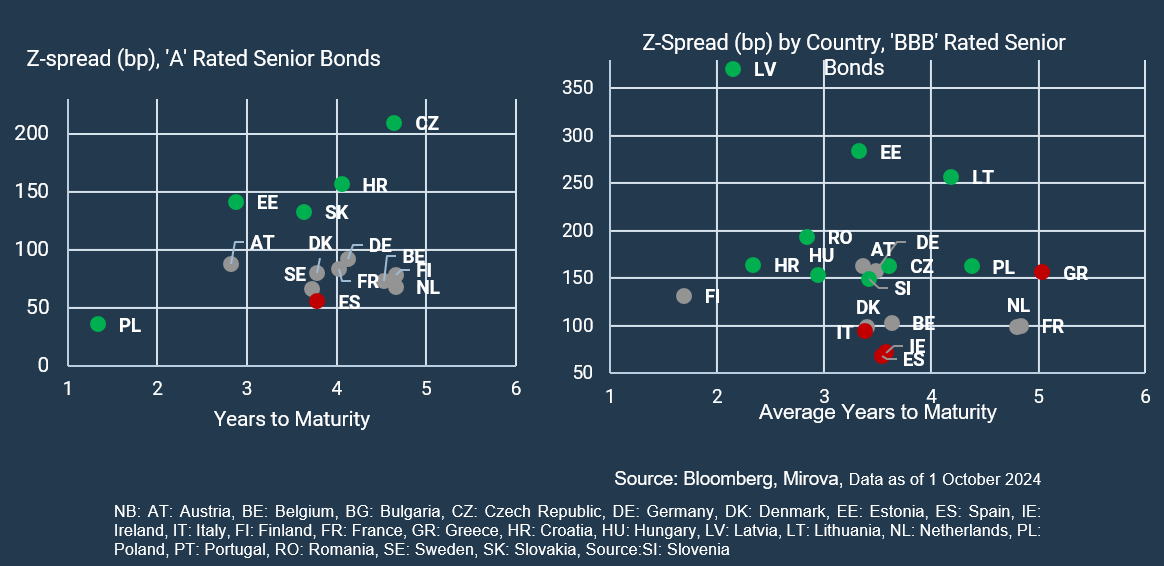

We find it interesting to note the spread differentials for senior bonds issued by CEE banks compared with those from Italy and Spain. The average spread premium is about 70 basis points18 for BBB-rated CEE bank senior bonds, excluding the Baltics, relative to Italian senior bonds in the same category, and about 95 basis points relative to Spanish peers. The Baltic banks offer the largest premium, likely reflecting the geopolitical risk in the region and the fact that most Western investors still do not have extensive knowledge of the sector.

In the 'A' category, Czech senior bonds issued by Moneta Money Bank AS are particularly attractive, providing a spread differential of about 180 basis points relative to similarly rated Spanish senior bonds. The premiums for Slovak and Croatian senior bonds also appear appealing relative to Western EU countries.

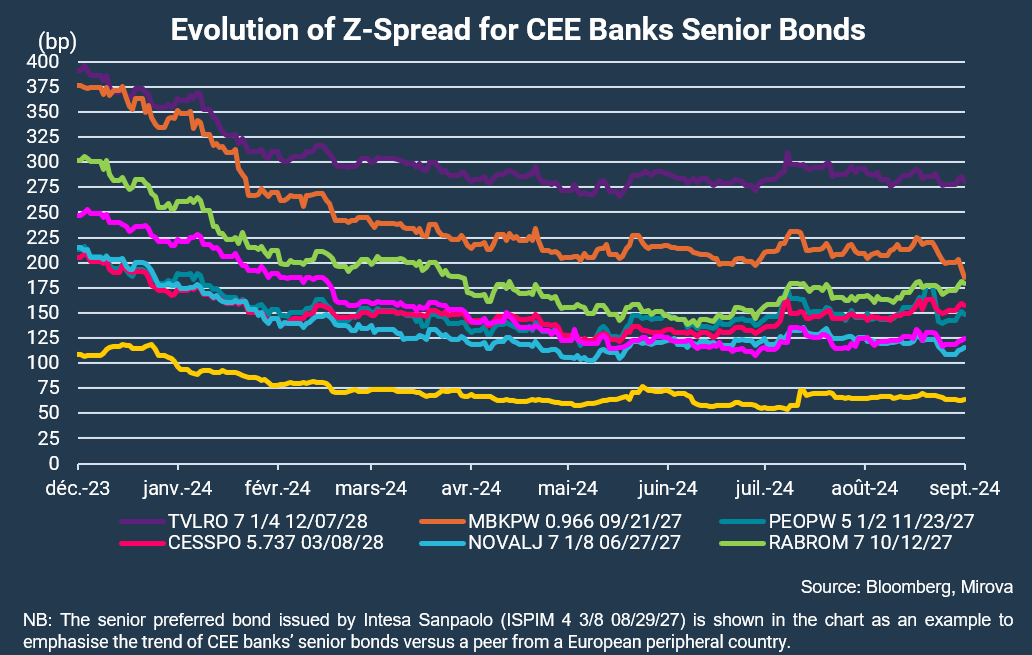

Between end 2023 and end September 2024, CEE senior bonds that are BBB-rated have outperformed their peers in Western Europe, with spreads having contracted by an average of almost 100 basis points19, compared to a contraction of about 36 basis points for Western European peers. We argue that there is still headroom for further spread tightening.

Economic Growth Prospects

Looking ahead, CEE banks are well-positioned to achieve profitable growth in the coming years, supported by the structural convergence of CEE economies with those of Western EU member states. Anticipated business volumes in 2024 and 2025 are expected to be bolstered by solid economic growth potential that exceeds the eurozone average, and the possibility of further rate cuts is likely to fuel credit demand. Additionally, banks should benefit from increasing banking penetration in the region and the broader availability of ancillary investment and savings products and services to customers.

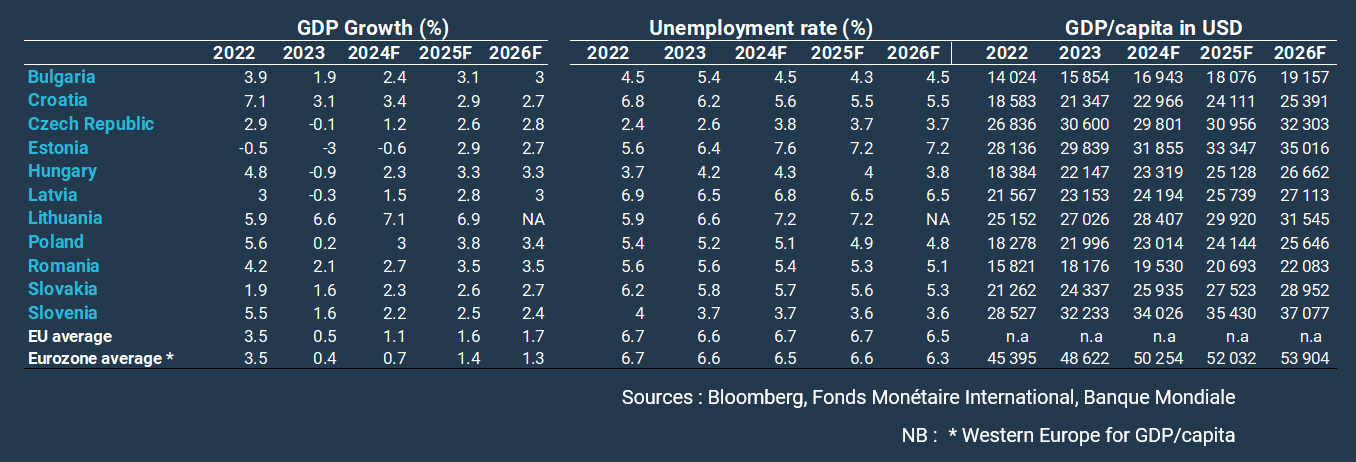

After a period of slowed growth momentum, economic activity in CEE countries is rebounding in 2024, and this growth is expected to continue into 2025. CEE countries are anticipated to grow at a faster pace than the EU average, with real GDP growth generally expected to be around twice as high as the average for the EU area. Estonia is an exception as the consensus expects the country to remain in recession in 2024 with a GDP growth forecast of -0.6%20 Czechia will grow in line with the average of the EU. We argue that EU funding and development programmes, including grants, loans, and guarantees, will continue to play a crucial role in enabling economic activity in CEE countries, contributing to the block’s digital, green energy, and social ambitions. CEE banks will indirectly benefit from the resulting economic growth and directly as intermediaries for EU funds to the recipients.

In addition to traditional EU funding, CEE banks' lending volumes will also be supported, albeit to a lesser extent, by programmes established by EU and non-EU institutions, such as the International Finance Corporation and the European Investment Bank Group. These programmes, including significant risk transfers transactions (synthetic securitisations), are aimed at expanding lending to small and medium-sized enterprises and sustainable project finance. This suggests that CEE banks will have opportunities to increase their lending activities and contribute to the growth and development of the region's economies, which will in turn will end-up reinforcing their credit profile.

CEE Banking Sectors - Similar but not the Same

Though the economic trend is similar across the whole CEE region with regards the expected sound GDP growth and stable unemployment, there are significant discrepancies in economic performance and banking sectors. Banks in the Czech Republic and Slovenia benefit from a strong record of economic performance, with the highest GDP per capita within the CEE region, estimated at about $30,000 and $34,000, 21respectively, in 2024, according to the IMF. These countries also have healthy public fiscal positions. The banking sectors in these countries are concentrated, which ensures strong pricing power for the dominant banks.

The Czech Republic has the second-largest banking sector in the CEE region, after Poland, but it accounts for only 1% of EU banking assets. However, it boasts the highest level of financial intermediation in the region, as measured by the ratio of financial system assets/GDP, which stood at 163%22 at the end of 2022, yet lagging the eurozone average of 516% for eurozone. The Czech banking sector is sound and stable supported by good record of macroeconomic performance, sound public finances and institutions. The Czech banking sector is 90%22 foreign owned. Furthermore, Czech banks' ratings are not constrained by those of their sovereign. The Czech Republic is rated Aa3/AA- by Moody's and S&P, at par with France.

Banks in Romania and Hungary operate in more volatile political environments and weaker public finances than peers, but they have fared well so far and exhibit sound structural fundamentals that compare well with the EU peers. The high degree of foreign ownership and the involvement of the European Bank of Reconstruction and Development as a long-term equity and debt investor, along with an EU-aligned regulatory environment, are expected to continue supporting the stability of the banking systems in both countries. Romania and Hungary are among the fastest-growing economies in the EU, and low private sector leverage is expected to structurally support earnings growth for the banks in both countries.

In Romania, the consolidation of the banking sector is expected to be beneficial for profitability and cost efficiency, further supporting the already high profitability. Additionally, Romania has the highest proportion of underbanked individuals in the EU, providing significant growth opportunities for banks in the country.

Poland boasts by far the largest economy, with 37 million inhabitants22, and banking sector in CEE, accounting for 2%22 of EU banking assets. The banking sector in Poland is more fragmented compared with other CEE countries, with a mix of foreign and domestically owned commercial banks, cooperative banks, and credit unions. However, the top five largest banks hold a dominant share of the market. The country's political and economic environment shares similarities with those observed in Romania and Hungary, characterised by a polarised political landscape, tense relationships with the EU, and a wide public deficit.

Despite these challenges, the Polish banking sector has shown good profitability and cost efficiency, supported by strong digital capabilities, promising growth prospects, adequate funding and liquidity, and a sound level of solvency. However, high government intervention and ownership, including in the two largest banks, are considered weaknesses from a governance and earnings perspective. Thank to adequate profitability, banks should be able to absorb the remaining legal costs from the legacy Swiss Franc mortgage loans and extraordinary costs related to the ongoing mortgage holiday scheme..

An investment case to consider

The combination of solid fundamentals, regulatory support, and attractive yield differentials makes CEE banks an appealing investment choice for fixed income portfolios. As the region continues to grow and integrate with the broader European market, the potential for enhanced returns without significant risk exposure presents a unique opportunity for investors. It’s happening in the East.

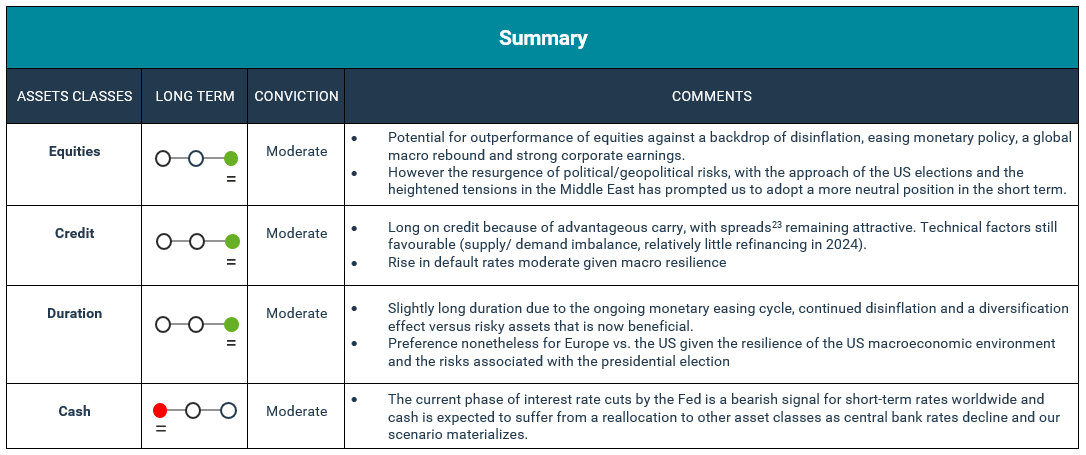

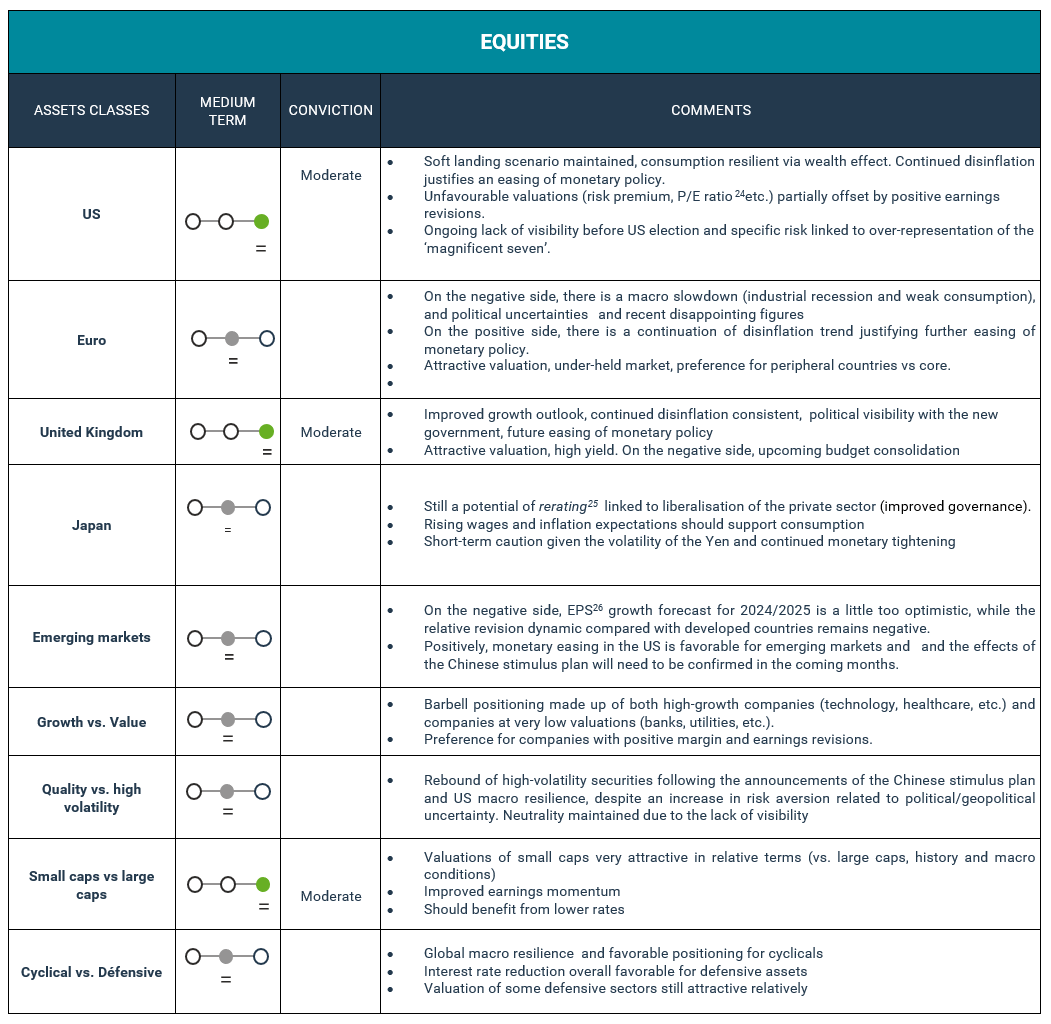

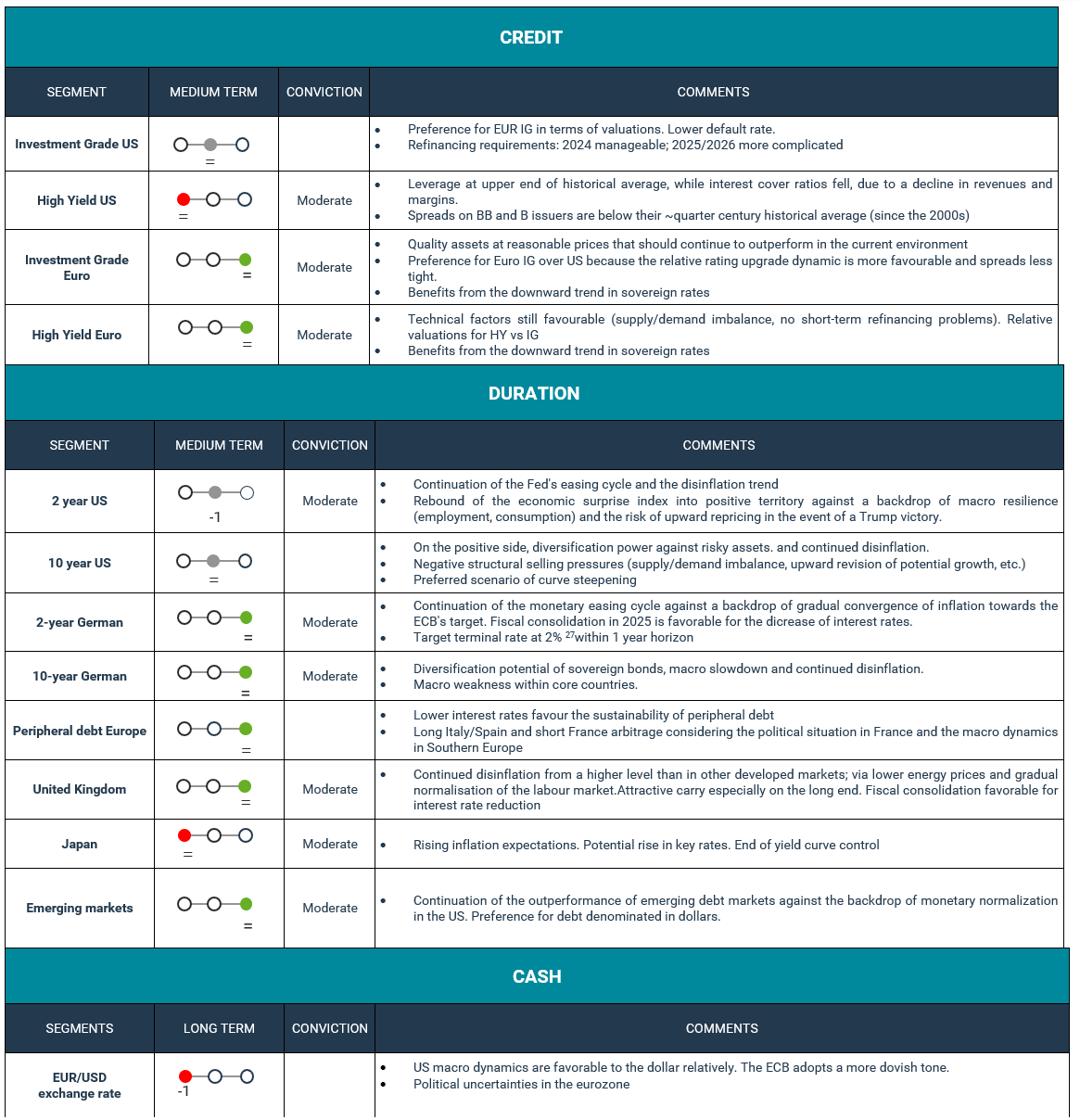

Summary of Market views

1Stock market index based on 500 large companies listed on US stock exchanges. The index is owned and managed by Standard & Poor's.

2Source: Bloomberg

3Purchasing Managers' Index is a composite indicator of a country's manufacturing activity.

4Difference between a bond's interest rate and that of a benchmark bond with the same maturity.

5USA Federal Reserve Bank

6Basis points

7European Central Bank

8Source: Bloomberg

9Source: Bloomberg

10European Union

11Source: Bloomberg

12Exchange Traded Funds

13Peripheral European countries refers here mainly to Spain, Italy, Ireland, and Portugal

14Core European countries mainly refer here at France, Belgium, Netherlands, Germany, and the Nordic countries.

15Source : Bloomberg

16Source : Bloomberg

17Long-term financing regulation in Poland requires banks to fund 40% of their residential mortgage loans granted to individuals with long term funding sources having a maturity of more than one year. Banks should favor covered bond issuance.

18Data as of 1 October 2024, Reference rating used is the Bloomberg Index Rating

19Source : Bloomberg

20Source : Bloomberg

21Source : Bloomberg

22Source : Bloomberg

23The spread is the difference between the two prices of an asset in the financial sector, namely the price at which a security is presented for sale, and that at which a buyer offers to purchase it, respectively the ask price and bid price.

24Indicator used in financial and stock market analysis.

25Re-estimation

26Earnings per share

27Source : Bloomberg

The information given reflects Mirova's opinion and the situation at the date of this document and is subject to change without notice. All securities mentioned in this document are for illustrative purposes only and do not constitute investment advice, a recommendation or a solicitation to buy or sell.